Why AML Documentation is Critical for Compliance

Record-keeping requirements are the „law of the land” in Anti-Money Laundering (AML) compliance, because „if it isn’t documented, it didn’t happen”. For many companies, documentation is the only shield standing between a smooth-running operation and a catastrophic regulatory crackdown, as fines issued to financial institutions only in the first half of 2025 reached approximately $1.23 billion. And most of these penalties resulted not from criminal activity, but from simple, avoidable gaps in record-keeping and due diligence.

This article sheds light on the essential AML documentation requirements, explains why record-keeping matters, and outlines best practices to help B2B companies build resilient compliance frameworks.

Core AML Documentation Requirements

Just as when building a house, you start by laying a solid foundation; in business, it’s your documentation that helps you build a robust Anti-Money Laundering program. Without it, the entire structure will crumble under the weight of an AML audit. To stay compliant, you need to track everything from who your customers are to how your employees are trained.

Customer Identification and Customer Due Diligence (CDD)

Before you sign a contract or process a payment (enter into a relationship with a customer or partner), you need to know exactly who is on the other side of the desk. And it’s customer due diligence that represents a living record of this relationship.

Here is a list of key documentation:

- Identity verification documents. You must maintain clear copies of government-issued IDs, such as passports, national IDs, or driver’s licenses.

- Proof of address. Validating a customer’s physical presence through utility bills or bank statements (usually no older than 3-6 months) is standard.

- Ultimate Beneficial Owner (UBO) records. For B2B companies, you must peel back the layers to find the humans who actually own or control the business (beneficial owners), typically anyone with a 25% or more stake.

- Customer risk profiles. Every client needs a risk rating; for example, low, medium, or high. High-risk clients require Enhanced Due Diligence (EDD), which involves more detailed documentation of their source of wealth.

- Politically Exposed Persons (PEP), terrorist financing, and sanctions lists. You must document any changes to your customers’ information that was gathered during ongoing monitoring.

EXAMPLE: If you are onboarding a tech company that is based in a high-risk jurisdiction, your file should include not just their articles of incorporation, but also a memo explaining why their business model makes sense and where their startup capital originated.

Transaction Records

Regulators want to be able to reconstruct any transaction in order to see where the money came from and where it went. That’s why you’re required to maintain clear records of your financial activity.

Here is what transaction monitoring includes:

- Payment details. Dates, amounts, currencies, and the specific accounts involved.

- Source of funds. Salary, business revenue, etc.

- Purpose of funds. A record of why the transaction happened. For example, „payment for Q3 software licensing”.

- Investigation logs. If a transaction was flagged by your system but cleared after review, you must document why you decided it wasn’t suspicious.

Suspicion and Investigation Reports

When things look strange or suspicious, your internal record trail becomes your best defense and the best tool for financial crime and fraud prevention. When things like that happen, the required records include:

- Internal notes. Document the initial „trigger”; for example, a client suddenly tripled their usual transaction volume.

- SAR submissions. If you file a Suspicious Activity Report (SAR), you must keep a copy of the report and any correspondence with the regulator, like the Financial Crimes Enforcement Network (FinCEN) in the US or a Financial Intelligence Unit (FIU) in your local region.

- Escalation steps. Show the timeline of who reported the activity and who made the final call to alert authorities.

Banks, savings associations, and credit unions alone submitted more than 2.193 million SARs in 2025 – a 7.66% increase from 2024. Source

Risk Assessments and Policies

Anti-money laundering compliance is always risk-based. That’s why your documentation must demonstrate that your approach is structured and intentional. Here are the essential documents that help assess AML risks effectively:

- Internal AML policy and procedures. This document outlines your company’s specific approach to preventing financial crime.

- Risk appetite statement. A formal record of what types of clients or industries your company is (or isn’t) willing to work with.

- Business-wide risk assessments. A comprehensive evaluation of your organization’s exposure to money laundering risks with regard to customers, products, geographies, and delivery channels.

- Policy updates and revisions. Documented changes to AML policies that reflect regulatory updates, emerging risks, or internal improvements. These ensure your compliance framework stays current and effective.

- Board and senior management approvals. These documents show evidence that senior management has reviewed and signed off on these policies annually.

EXAMPLE: If your company expands into a new market, your risk assessment should reflect new exposure; for example, higher corruption risk. The updated policy and approval must then be documented.

Training and Compliance Records

Your business can stay compliant and fraud-resistant only if your employees are trained to spot red flags in customer and partner behavior. And regulators expect to see proof that your employees understand anti-money laundering obligations.

Policy acknowledgments. Digital signatures from every staff member confirming they have read and understood the latest AML updates.

Training logs. Records of who attended the AML training, when it happened, and what was covered, including the logs of refresher training sessions.

Certifications and test results. Results from quizzes or tests that prove employees actually understood the material.

Why AML Record-Keeping Matters

Record-keeping is the backbone of any successful AML solution. It serves as a comprehensive documentation system that not only ensures compliance with regulatory requirements but also acts as a valuable resource for internal investigations and audits.

Let’s review the main benefits of keeping AML documentation:

Meeting Regulatory Obligations

Global AML frameworks and regulatory bodies, such as the Financial Action Task Force (FATF), require you to keep records for a specific period.

- In the EU, under the latest AML Directives (AMLD6), the standard retention period is also 5 years after the business relationship ends.

Failure to meet these legal and regulatory requirements is a common reason for penalties.

Supporting Internal Investigations and Audits

Regulators always demand proof of your financial activities in the form of an audit trail. Detailed records allow you to prove that you conducted your customer due diligence at the time of onboarding, not months later when a problem arose.

Good internal documentation allows your compliance team to reconstruct events quickly, identify patterns across customers or transactions, and make informed decisions. So, if multiple alerts involve the same counterparty, historical records help uncover a larger scheme.

And the audit trail shows regulators that your company monitors activity, applies a risk-based approach, and takes action when needed.

Assessing and Managing Risks

By looking at past records of flagged activities, your compliance team can refine its risk models and ensure your business’ future security. Of course, risk levels vary marginally across jurisdictions and depend on factors like transparency, corruption levels, and legal systems that you have in place. But one thing is sure – detailed historical records will help you:

- refine risk scoring models,

- identify high-risk segments,

- improve onboarding and transaction monitoring rules.

Using Standardized Templates and Version Control

When it comes to documentation, consistency can hardly be overestimated. If every compliance officer uses a different format for their notes, your data becomes a mess. Using standardized templates ensures that no critical questions are missed during onboarding, and version control shows auditors that you are constantly updating your processes to meet new threats.

„The aim of AML regulation is not to catch anyone out but to set high standards of probity and scrutiny to inhibit illicit money flows in the financial system and to encourage participants in the system to behave as custodians and guardians of the public interest in preventing money laundering.” – Mark Steward, Executive Director of Enforcement and Market Oversight, Financial Conduct Authority

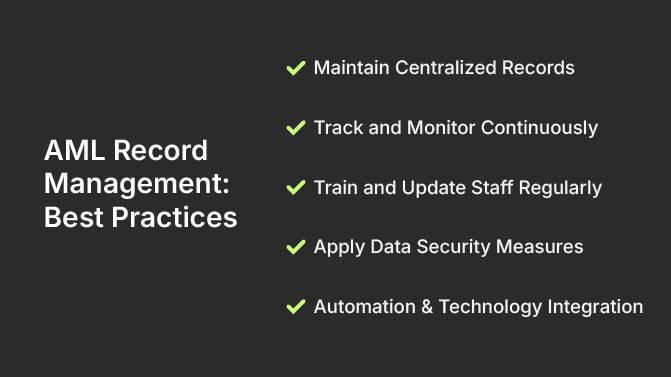

Best Practices for AML Record Management

Now that we understand the significance of record-keeping in AML processes, let’s explore some best practices.

Maintain Centralized Records

Storing your customer information in scattered spreadsheets is not a good idea. It’s better to use a centralized, digital repository that links all Know Your Customer (KYC) and transaction data. So, if an auditor asks for information on „Client X”, you should be able to pull their entire history in seconds.

The benefits of having a centralized system of records are:

- Faster access during audits

- Reduced duplication

- Better cross-team collaboration

Track and Monitor Continuously

AML is never static. It’s rather a dynamic system. So, it’s advisable to set up systems that alert you whenever a customer profile changes: when an ID has expired or a company’s business structure changes. This will help you detect suspicious transactions or activities earlier.

Train and Update Staff Regularly

Regulations change, like, for example, the recent transition to AMLD6 in Europe. Make sure your team isn’t working off an old playbook. To ensure your employees stay in the loop on recent events and reduce human error, it’s best to conduct regular training, inform them of new risks and regulations, and, of course, continuously test their knowledge.

Apply Data Security Measures

AML records contain highly sensitive Personal Identifiable Information (PII). Encryption, audit logs, secure backups, and strict „need-to-know” access controls are non-negotiable to prevent data breaches.

Automation and Technology Integration

Manual record-keeping often leads to human error. Modern financial institutions use automated solutions to flag UBO changes, screen against sanctions and terrorist financing lists in real time, and archive documents with timestamped precision. And modern AI tools help reduce false positives.

Final Thoughts

Documentation is your company’s memory. In a regulatory environment, your records are the only evidence that counts. By investing in robust AML record-keeping today, you’re future-proofing your business.

It’s paramount to keep your records and reporting systems up to date, because this way you’re always following the latest rules. Switching to digital AML tools is a great way to speed things up. Above all, don’t hesitate to report anything that looks suspicious, as it’s the best way to keep your business out of trouble.

FAQ