Understanding Suspicious Activity Reports (SARs)

Financial crimes such as money laundering, fraud, and terrorist financing pose significant threats to global security and economic stability. To combat these illicit activities, financial institutions rely on a critical mechanism known as a Suspicious Activity Report (SAR). According to the Financial Crimes Enforcement Network, financial institutions have filed more than 24 million SARs since 1996 up till now.

In this article we will explore what suspicious activity reports are, why they matter, and how the filing process works.

What Are Suspicious Activity Reports (SARs)?

Each time a financial institution, like a bank, detects potential illegal or suspicious activity involving their accounts or services, they must submit a suspicious activity report. This report is usually filed with the Financial Crimes Enforcement Network (FinCEN) in the US or an equivalent regulatory body in their country.

The main purpose of a suspicious activity report is to alert authorities, so they can investigate and prevent financial crime. SARs are submitted to the local Financial Intelligence Units (FIUs) – government agencies tasked with analyzing such reports.

Outside the US, SARs are often referred to as Suspicious Transaction Reports (STRs), but they serve the same function: to flag suspicious financial behavior. For example, the UK’s National Crime Agency (NCA) receives STRs under the Proceeds of Crime Act.

Who Must File SARs and Who Regulates Them?

SAR filing responsibilities fall primarily on financial institutions, such as banks, credit unions, money services businesses, FinTech platforms, and broker-dealers – basically, any entity that handles money or assets.

Suspicious activity reports are regulated under the Bank Secrecy Act (BSA) of 1970. Initially referred to as a “criminal referral form”, the SAR became the standard method used to report suspicious activity in 1996. Primarily, SARs assist financial institutions in identifying and reporting known or suspected violations. But the USA PATRIOT Act later expanded SAR requirements to address both domestic and global terrorism.

In the US, the FinCEN is the FIU that oversees SAR filings. Other countries have similar agencies, such as the NCA in the UK or the FIUs designated by the Financial Action Task Force (FATF) member nations. Each jurisdiction has its own timelines, formats, and e-filing portals, which institutions must follow strictly.

Why Are SARs Important?

Early detection of financial crimes. SARs help identify suspicious transactions quickly, stopping illegal money from moving through the financial system. By flagging suspicious transactions, financial institutions help law enforcement agencies in their efforts to combat money laundering, fraud, and terrorist financing.

Ensuring compliance. Filing SARs is a legal requirement for financial institutions under Anti-Money Laundering (AML) laws and regulations. Non-compliance could result in civil and criminal penalties as well as reputational damage.

Law enforcement support for investigations. SARs provide crucial information that helps police and other law enforcement authorities investigate and catch criminals.

Maintaining financial system integrity. SARs protect the trust and stability of banks and markets by preventing abuse.

What Constitutes Suspicious Activity?

The red flag, suspicious activities can be named broadly as unusual transactions, which do not fit the customer’s normal behavior or business profile, such as sudden large cash deposits or withdrawals, frequent transfers to foreign accounts, or transactions just below reporting thresholds.

Financial institutions are trained to identify a wide range of suspicious transactions and activities. Here is an overview of some of the common indicators that your company must submit suspicious activity reports:

Structuring – a deliberate attempt to evade reporting requirements by breaking down large transactions into smaller, seemingly unrelated ones, or the use of multiple accounts to move funds in a way that obscures the origin or destination.

EXAMPLE: A bank notices repeated cash deposits just below the $10,000 reporting threshold across multiple accounts tied to the same business. After investigation, the bank suspects structuring and files a SAR detailing transaction patterns, timelines, and parties involved.

Unusual business practices, such as activities in dormant or rarely used accounts, including rapid movement of funds after long inactivity, or large wire transfers to or from high-risk jurisdictions without clear business reasons.

Other red flags in customer behavior, such as being reluctant to provide necessary information, offering vague explanations of their transactions or sources of funds, transactions lacking any apparent legitimate business or lawful purpose, or activities involving unlicensed or unauthorized money services or suspicious use of financial products.

EXAMPLE: If a customer who regularly deposits $500 monthly suddenly makes weekly transfers of $9,000 and immediately withdraws the funds, this strange behavior could trigger a SAR filing, because it deviates significantly from their normal patterns and may suggest layering of illicit funds.

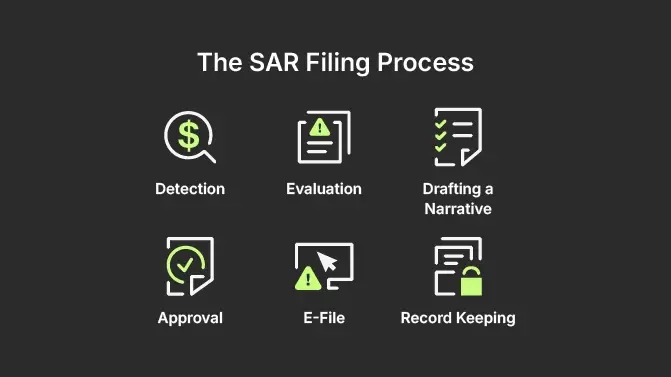

The SAR Filing Process

- DETECTION – Identify suspicious behavior or transactions

The first step involves using internal ongoing monitoring systems, red flag indicators, and staff observation to spot activity that is unusual for a customer, inconsistent with their known business, or appears to be an attempt to evade reporting requirements (like structuring transactions below a threshold). Timely detection is crucial to meet reporting deadlines.

- EVALUATION – Assess the risk and gather relevant information

Once suspicious activity is detected, a compliance or internal investigation team reviews the activity, accounts, and customer history. At this stage, the goal is to determine if the activity meets the threshold for filing a suspicious activity report and to collect all supporting documentation, such as account statements, wire transfer details, dates, amounts, and identifying information for all parties involved.

- DRAFTING A NARRATIVE – Compose a clear, detailed description of the suspicious activity

Being the most critical part of the report, the SAR narrative must present a complete, chronological account of the facts, explaining why the activity is suspicious. It should explain who did what and when exactly, while avoiding speculation and clearly referencing the supporting documents. A strong narrative is essential for law enforcement and regulators.

- APPROVAL – Review and approve the SAR internally

Before submission, the draft of a suspicious activity report and its supporting documentation must be reviewed by designated personnel, such as a compliance officer or legal counsel, to ensure accuracy, completeness, and adherence to regulatory standards. This internal quality assurance step mitigates the risk of submitting a deficient or non-compliant report.

- E-FILE – Submit the SAR using mandated e-filing systems

The approved SAR is submitted electronically to the relevant financial intelligence unit, like FinCEL in the US, using a secure, designated system (like the BSA E-Filing System). Filers must adhere to the strict reporting deadline, which is typically 30 calendar days after the initial detection of the facts that constitute a basis for filing.

- RECORD KEEPING – Keep SAR copies and supporting documents securely as required by law

The reporting institution is required to save a copy of the SAR filing (either in a paper or electronic format) and all the supporting documentation for a specified period, typically five years from the date of filing. These records must be kept confidential and are provided to regulatory or law enforcement agencies upon request.

How to Write a Strong SAR Narrative

The narrative of a suspicious activity report should follow the classic 5W1H format.

- Who: Parties involved

- What: Nature of the suspicious activity

- When: Dates and times

- Where: Locations or accounts

- Why: Explanation of why the activity is suspicious

- How: Methods or techniques used

Include amounts, counterparties, typologies (for example: structuring, sudden large deposits, unusual behavior), and any investigative steps or remedial actions taken.

An example of a SAR narrative

Summary of Activity:

On August 5, 2025, our compliance team identified a series of unusual transactions on the account of Steven Wright, a customer of X Bank. Between July 28 and August 3, 2025, the customer made five cash deposits totaling €45,000, each under the €10,000 reporting threshold.

- Deposit 1: €9,000

- Deposit 2: €9,500

- Deposit 3: €9,200

- Deposit 4: €8,800

- Deposit 5: €8,500

Total: $45,000

The deposits were made at different branches of the X Bank within short time intervals.

Background:

Steve Wright opened the account on May 15, 2025, declaring his occupation as a freelance consultant with an expected monthly income of €3,000–€4,000. The account had minimal activity prior to these deposits.

Details of Suspicious Activity:

The structured nature and frequency of deposits suggest an attempt to avoid currency transaction reporting requirements (structuring/smurfing). No business activity or legitimate explanation was provided for the sudden influx of cash. When contacted on August 6, 2025, the customer stated the funds were from “friends”, but declined to provide supporting documentation.

Conclusion:

Based on the transaction pattern, inconsistent customer profile, and lack of a verifiable source of funds, this activity is suspected to involve possible money laundering. SAR submitted for further investigation.

Confidentiality and Safe Harbor

Suspicious activity reports are kept strictly confidential for a good reason. To make sure these reports actually work, financial institutions and their employees can’t tell anyone about the filing of a SAR, especially to the person being reported. This is a breach called “tipping off”, and it can wreck investigation, undermining the work of law enforcement authorities, who are responsible for stopping money laundering.

On the flip side, the people filing these reports usually get legal protection through “safe harbor” laws, which shield them from civil or criminal liability when filing reports in good faith. The rules differ depending on where you are, but the idea is the same: make it safe for banks and employees to flag sketchy, possibly criminal behavior without worrying about getting dragged into court.

Keeping things confidential also protects everyone involved: the people under investigation don’t have their names dragged through the mud prematurely, and the whistleblowers or compliance agents who report suspicious activity. That’s why before a SAR goes out, it usually gets reviewed by management and lawyers to make sure everything’s accurate and properly handled.

Without confidentiality and legal protection, people would be too scared to report suspicious activity, and financial crimes would flourish.

Challenges and Best Practices

First, let’s highlight the challenges financial institutions face when creating suspicious activity reports.

- Transaction monitoring systems often flag many legitimate transactions as suspicious (false positives), overwhelming compliance teams and creating backlog delays.

- Money launderers and fraudsters continuously adapt their methods and tactics, which requires constant updates to detection rules and monitoring techniques.

- Organizations must navigate complex and strict filing requirements from regulators, including tight deadlines (often within 30 days) and jurisdiction-specific rules, risking penalties if deadlines or quality standards are missed.

- Incomplete or inaccurate customer and transaction data can hinder investigations and lead to weak or rejected SARs.

- Protecting information and preventing tipping off subjects remains a sensitive and critical aspect of the entire SAR handling.

Second, to overcome these SAR filing challenges and successfully prevent money laundering, businesses are advised to adopt the following best practices:

- Consistent employee training on red flags and procedures.

- Strong governance and regular quality assurance reviews.

- Maintaining high data quality and updating watchlists.

- Having a clear escalation procedure for suspicious cases.

- Regular feedback loops with law enforcement to improve report quality.

Looking into the Future

Helping banks and other financial institutions spot and report strange behaviors, suspicious activity reports are a critical tool in fighting financial crime. In fact, millions of SARs are filed every year, with a huge chunk related to fraud, identity theft, and cybercrime. Making sure illicit funds don’t slip through the cracks, SARs are vital in catching money laundering, fraud, and even threats to national security.

The future of SAR reporting is deeply intertwined with advancements in technology. Artificial intelligence and machine learning are increasingly used to automate the detection of suspicious transactions, thus improving accuracy and reducing false positives.

AI systems will soon be able to create SARs automatically, spot complicated patterns, and help banks figure out which cases need attention first. AI is also likely to get better at reading things like transaction notes and messages to understand what’s really going on, making the reports more accurate and useful.

FAQ