Everything You Need to Know About the KYC Process

Whenever your business needs to implement identity verification processes for customers, it might feel like an operational burden, but there’s a good reason for it: fraud has become a bigger deal than ever before. Every day billions of dollars are moved around the globe, and a lot of that money is tied to illegal activity. And financial institutions are facing serious consequences if they fail to detect and prevent fraudulent activities.

To effectively weed out financial crimes, regulators are getting tougher by introducing giant penalties. One of the biggest reasons for businesses getting hit with massive fines is not knowing who their customers really are. That’s why the Know Your Customer process has never been as important as it is now.

What is KYC?

Know Your Customer (KYC) is a set of regulatory procedures used to verify a customer’s identity and determine what fraud risk they may pose. Many financial institutions turn to KYC processes to assess money laundering risks.

KYC compliance has always been a concern for financial institutions like banks, online payment platforms, and insurance firms. However, they’re not the only ones that should care. The number of industries that must comply with the KYC process and perform customer due diligence is expanding. Organizations that provide healthcare, gambling, telecommunications, and many other services must comply with Know Your Customer compliance standards.

Why is KYC important?

Fact: we live in a world where financial crimes like fraud, money laundering, and identity theft are rampant. In 2024 in the US alone, the value of Anti-Money Laundering (AML) fines for financial institutions reached $3.3 Billion. Not surprisingly, KYC has become a critical part of AML compliance.

Generally speaking, KYC regulations help institutions verify customer identities, assess risks, and prevent illicit activities. In practice, implementing a KYC process:

- Helps banks reduce exposure to financial risk and identify potential money laundering activities.

- Keeps customer data accurate and helps detect suspicious activity on time.

- Helps prevent identity theft and enhances security.

- Protects institutions and clients from reputational damage.

There are three major benefits of KYC. First, regulatory compliance – KYC procedures are essential for financial institutions to meet standard compliance obligations. KYC compliance failures lead to hefty fines and severe penalties. Second, risk management – KYC allows institutions to understand who they’re doing business with, assess potential risks, and stop illicit activities before they even start. Third, reputation and trust – a robust KYC process signals customers that they can trust you with their money, and that it’s protected from criminal activity.

In a nutshell, KYC isn’t bureaucracy – it’s the foundation of a safe financial world.

Types of KYC processes

KYC can be divided into two main types: digital or eKYC and in-person verification.

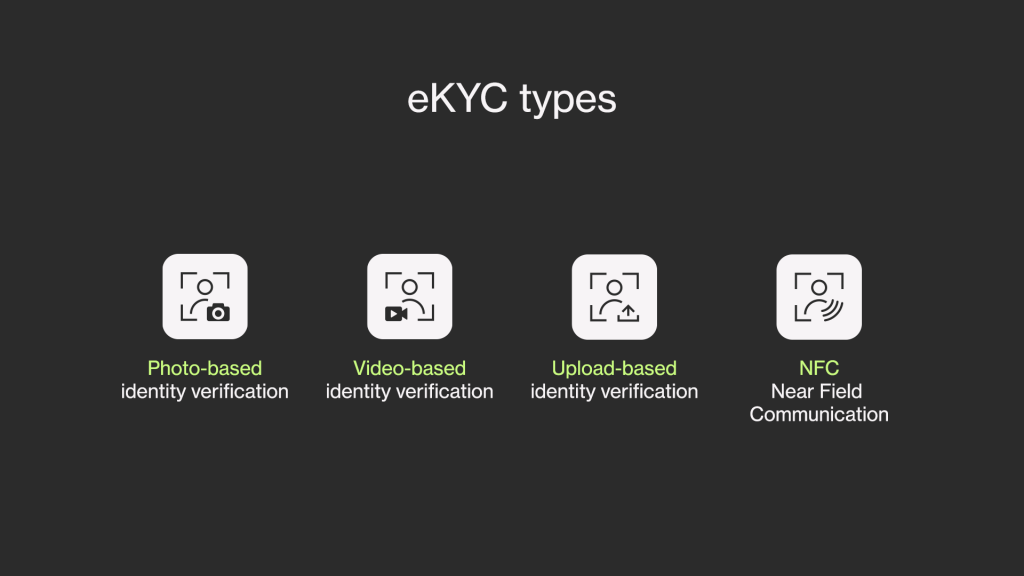

eKYC

eKYC is a digital KYC procedure, also known as an automatic identity verification process. It allows financial institutions to onboard clients in real time without compromising security. All necessary checks can be performed in the background with one customer identification program.

Various technologies can help improve the eKYC process. Customers can save time with OCR mode, which automatically extracts information from their IDs. Liveness detection can ensure that a person is present during the process, and the AML ongoing monitoring minimizes any future risk.

Photo-based KYC

This is a familiar and rather simple KYC onboarding process for clients. While the steps a client has to take vary depending on local regulatory requirements, the Ondato solution onboards customers in 2 steps:

- They take a selfie. Then, the system performs a liveness check and maps out their biometric data.

- The client takes a picture of their document.

In the background of the process, the client’s data is checked against numerous ID registries to confirm its authenticity and KYC compliance. The process usually takes around 30 seconds.

Video KYC

The Video KYC method is an assisted identity verification done in real-time via a video call. A customer’s biometric and document data is captured during an encrypted call. The KYC specialist may ask further questions to ensure that the client is who they claim to be. The video call is then analyzed for possible spoofing attempts, ensuring that no fraudster can fool the KYC specialist or the system. The process is completely secure and establishes a personal connection with the customer to enhance their experience with KYC processes.

Document-based KYC

Also known as an upload-based identity verification, this is a process that allows users to submit data manually via document upload. This type of the KYC process can be used when the KYC regulations allow the client to not be present during the verification process. The document-based verification method can replace real-time procedures while staying compliant with KYC requirements.

NFC (Near Field Communication) Verification

This method allows compatible devices to extract and wirelessly transfer data from microchips. It is used as an efficient security measure that provides fast customer onboarding by extracting the information from ID documents.

In-Person Verification

In-Person-Verification, also known as Manual Verification, refers to a physical KYC process. A customer must physically deliver relevant KYC documents, such as their ID, proof of address, etc. The KYC specialist will then run the data against various registries to confirm authenticity.

Digital vs In-Person KYC: Key Differences

Gone are the days when only a human could verify the authenticity of an ID. Today, technology can be just as effective. However, KYC regulations require financial institutions to combine these two types. Let’s discuss why that’s a good idea.

Cost

Physical KYC verification is resource-intensive, requiring significant investment in labor, office space, and technology. For instance, we have estimated that big banks in Germany, the Netherlands, France, and Switzerland spend an average of €5.7 million annually on KYC, with 74% of that cost allocated to labor. Automating the identity verification process with solutions like Ondato can reduce costs by over half, with a single verification costing less than €1. The price can be even lower depending on the number of verifications you need to perform.

Processing Time

Fast onboarding is key to customer satisfaction. Traditional, paper-based KYC checks can take up to 18 minutes, whereas automated systems like Ondato complete the process in under 30 seconds. A single human KYC specialist can perform only about three checks per hour, but Ondato can verify up to 50 users in the same amount of time.

Success Rate

Manual KYC checks are prone to human error from fatigue or lack of training, making them inefficient. The most effective approach combines human oversight with technology. Modern KYC technology uses biometrics to detect spoofing attempts (like masks) and analyzes documents for alterations, resulting in a 99.8% success rate.

What is the Difference Between KYC and KYB?

Know Your Customer and Know Your Business (KYB) are similar concepts, yet they should not be confused. While both procedures are verification standards, they deal with different entities.

KYC applies to an individual, such as a person trying to open a bank account. They protect financial institutions against money laundering, corruption, and fraud from their individual clients. This process requires several steps to understand the nature of customer activity, establish identity and ensure their funds are legitimate. Meanwhile, KYB checks are performed on business organizations. This involves the due diligence review of any business that a company works with. KYB processes establish the company’s identity and authenticity to ensure AML compliance.

What is the KYC Process?

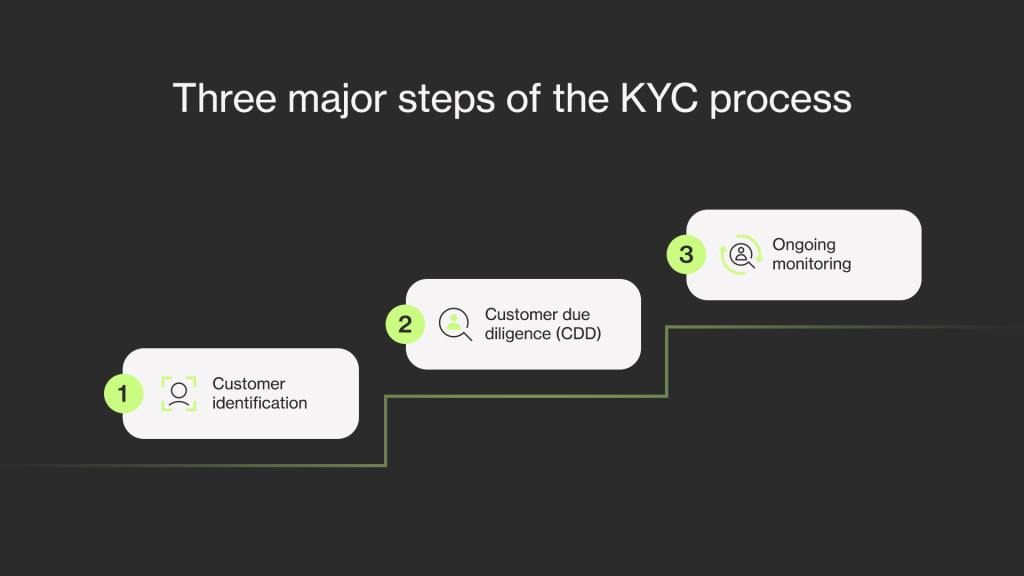

The KYC process involves three major steps:

STEP 1. Customer identification: a customer’s identity is verified by checking the provided documents.

STEP 2. Customer due diligence (CDD): a process that involves the collection of all needed data about the customer. The data is gathered from verified and reputable sources to analyze the risk factors of the customer. Full compliance is ensured by taking additional steps:

- PEP screening: a customer’s name is checked against the Politically Exposed Person (PEP) lists to evaluate their risk score. According to international standards, a person involved in politics is deemed to be more susceptible to corruption. Thus, their risk score is higher.

- Sanctions screening: a customer is checked to ensure that they do not appear on a sanctioned entity list.

- Adverse media screening: a customer’s reputation is reviewed by scanning through media outlets.

- If these checks result in a higher risk score, Enhanced due diligence (EDD) should be performed. For example, high risk is assigned to politically exposed persons or those from high-risk countries. A deep investigation is performed on a customer during the process to evaluate possible fraud risks.

STEP 3. Ongoing monitoring: compliance does not end with the onboarding of a customer. To ensure that a customer remains who they say they are months after onboarding, their data should be subject to ongoing monitoring throughout the whole customer lifecycle.

What Is KYC Remediation?

A lot can change during a customer’s lifecycle. Once you onboard a client, you can never be certain they are still who they say they are a year later. That’s why regulated industries should re-validate their customers. This process is called KYC remediation. It ensures that your customer’s data is updated according to the most recent regulations and your KYC obligations are fulfilled.

Generally, remediation is performed in a 6 or 36-month cycle. However, it all depends on the client’s risk score: the higher the client’s risk, the shorter the remediation cycle.

KYC Remediation can be a complex and expensive procedure. To make the process easier, start the remediation with only high-risk clients. Firstly, identify the outdated and collect the missing data. Automated KYC software can help you gather this information much faster. Additionally, by enabling constant monitoring of your clients, you’ll know exactly which of them needs to be remediated. Ondato offers all the necessary KYC and data monitoring tools in one comprehensive suite. Stay compliant with current regulations and mitigate the risk of fraud with our customer data platform.

Who Needs to Perform KYC?

Financial institutions will always be at the center of KYC, but that doesn’t mean that KYC requirements do not apply to other industries.

Knowing who your clients are is not only useful to ensure your company’s integrity and reputation, but also to sift out those who shouldn’t be using your service. It is especially true for companies that offer age-restricted services and want to deter minors from using their platform. And having a comprehensive KYC checklist can help a lot with this process.

Here is a list of the most prominent industries subjected to KYC regulations:

- Finance

- Online gaming

- Gambling

- Alcohol sales

- Travel

- Virtual and Crypto wallets

- Telecommunications services

- Medical services

- Others

KYC Requirements for Businesses

KYC is now a core compliance requirement for any business that handles money. Knowing who you’re working with and verifying their identity by checking their name, address, date of birth and a government‑issued ID – is no longer a “nice to do” but rather a mandatory process.

After identification, firms perform customer due diligence to understand what the customer does and assess the risk of money laundering or financial fraud. High‑risk clients, such as those from sanctioned countries or using shell companies, require enhanced due diligence, which involves a deeper investigation into their background and the source of their funds.

But KYC doesn’t end at onboarding. Ongoing monitoring tracks transactions and triggers suspicious activity reports to regulators. These processes follow a risk‑based approach and rely on solid record‑keeping and training.

And the regulatory requirements for businesses are getting tougher each year. For example, in 2025 EU regulators tightened the rules even more. The EU’s new Anti‑Money‑Laundering Regulation lowered the threshold that triggers due diligence from €15,000 to €10,000, and now requires checks on cash transactions over €3,000.

This move is set to strengthen beneficial owner checks and expands the definition of politically exposed persons. Today, high‑value‑goods dealers, art galleries, crypto‑asset providers, and even football clubs fall under the same obligations as banks.

KYC: A Partner in Your Business’s Success

Rather than just being a tedious task that eats up time and money, a strong KYC process is a powerful way to protect your company’s reputation and bottom line from serious financial crime. Modern, smart solutions are completely changing the game by transforming a slow, manual process into a fast, secure, and even seamless part of your customer’s journey. Digital KYC not only drastically reduces processing times and human error but also enhances the overall customer onboarding experience, fostering trust from the very first interaction.

A customer identification program, like Ondato, is sure to make your KYC journey much more efficient.

FAQ