Money Laundering Red Flags in the UK: Key Warning Signs for Businesses

Money laundering rarely arrives with a clear label. Often, it looks like everyday business. And the scale of the problem is significant for the UK in particular, as the country processes trillions of pounds in financial flows every year, making it one of the most attractive targets for money launderers anywhere in the world.

Unfortunately, it is estimated that more than £100 billion is laundered annually through the UK or via UK corporate structures. For businesses, failing to spot the warning signs of financial crime is a major risk that may jeopardize their very existence. That is exactly why UK businesses need to recognize red flags early.

This article explores the specific money laundering red flags defined by UK regulators, outlines why they matter for your operations, and explains how your business can actively detect them before they lead to regulatory disaster.

What Are Money Laundering Red Flags?

Let’s start with a definition. The UK Anti-Money Laundering (AML) regulations define a “red flag” as any indicator, such as a behavior, a transaction pattern, a document inconsistency, or a customer characteristic, that suggests funds may be criminal in origin or that a customer may be attempting to disguise illicit money as legitimate.

Under the Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017 (MLR 2017), regulated businesses are legally required to identify these signals (red flags), conduct appropriate due diligence, and report suspicions to the authorities.

It’s important to note that red flags don’t automatically prove guilt, but they do trigger an obligation to look closer and, often, to act. In other words, red flags aren’t about certainty, but rather about reasonable grounds for money laundering suspicion. If something doesn’t add up, the UK’s anti-money laundering legislation expects you to investigate it.

Why Money Laundering Red Flags Matter for UK Businesses

As we’ve established so far – spotting money laundering red flags is a legal obligation in the UK. So, missing red flags can lead to legal, financial, and reputational damage.

According to the National Crime Agency (NCA), organizations and individuals in the regulated sector have a legal obligation to submit Suspicious Activity Reports (SARs) when required. Failure to submit a SAR when there is a legal obligation can lead to prosecution, regulatory action, up to five years’ imprisonment, a fine, or both.

Key UK anti-money laundering regulations and laws include:

Spotting red flags early gives businesses time to pause, check, document, escalate, and report where needed.

Common Money Laundering Red Flags in the UK

Criminals constantly refine their methods of trying to bypass traditional internal controls. To protect your business, you need to monitor transactional behavior, customer actions, and operational abnormalities across several distinct categories.

Typically, money laundering follows a three-stage process:

- placement – introducing illicit funds into the financial system

- layering – obscuring the trail

- integration – making the money appear legitimate

Since money laundering red flags can appear at any stage, here is what you need to watch for when it comes to transaction, customer actions, and operational activities.

Unusual or Suspicious Transactions

One of the clearest indicators of a money laundering red flag is economic in nature – unusual transactions. For example, those can be payments that do not match the customer’s profile, i.e. are inconsistent with a customer’s known business or income.

Other tell-tale signs of a suspicious transaction are rapid movement of funds, round-number transactions made frequently, unexplained third-party payments, or transactions with no clear business rationale or purpose.

And here is a real-life example of the consequences of failing to spot red flags for unusual transactions.

One of the most significant AML enforcement actions in UK history is the story of NatWest Bank, which failed to monitor the banking activity of a customer whose cash deposits escalated from normal levels to over £365 million over the course of 5 years, largely in cash-stuffed bags. The Financial Conduct Authority (FCA) fined NatWest £264.8 million in 2021. The escalating, unexplained cash volume was a classic transaction red flag that went unaddressed.

Large Cash Deposits and Cash Payments

Criminals love cash because it leaves no paper trail. Money-launderers often use the structuring mechanism to break down a large sum into smaller, frequent deposits and avoid triggering mandatory reporting thresholds.

Cash-heavy businesses, such as nail salons, car washes, restaurants, and takeaways, are frequently flagged in the NECC’s National Risk Assessments as being used as cover-ups for laundering, because their cash-based revenue is hard to independently verify.

In the UK, HM Treasury’s National Risk Assessment (NRA) of Money Laundering and Terrorist Financing reports high levels of cash-based money laundering, which involves using cash-intensive businesses and legitimate channels like local Post Offices to inject dirty cash into the banking system.

EXAMPLE: A newly onboarded corporate client operating a consulting firm frequently deposits £9,500 in physical cash across different bank branches every single week, intentionally keeping each deposit just under the typical threshold, which triggers deeper internal screening.

Multiple Bank Accounts and Complex Fund Transfers

Criminals frequently move money through an unnecessarily complicated network of accounts to break the audit trail. They split funds across different banks, jurisdictions, and account holders, making it incredibly difficult for standard monitoring systems to connect the dots – this is called “layering”.

The typical warning signs include:

- Multiple accounts held at different institutions with no clear business rationale

- Frequent transfers between accounts that serve no obvious commercial purpose

- Use of correspondent banking or offshore accounts in jurisdictions with weaker AML controls

- When funds are received and immediately moved elsewhere without any commercial activity in between

EXAMPLE: A property management company opens accounts at three separate UK banks and regularly transfers funds between them before paying contractors. When asked to explain the structure, the company’s directors cannot give a coherent business reason.

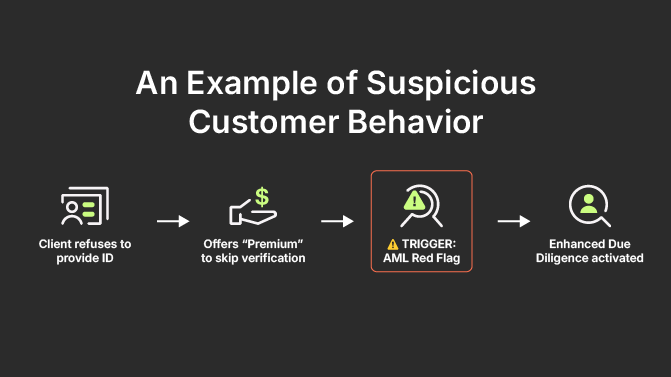

Suspicious Customer Behavior

Sometimes the red flag isn’t in the numbers but in how a customer behaves.

For example, customers may refuse to provide documents, pressure staff to move quickly, give inconsistent answers, become defensive when asked about funds, appear unusually knowledgeable about AML processes and reporting thresholds, or change their story.

His Majesty’s Revenue and Customs (HMRC) mandates businesses that have doubts or suspicions about a customer’s identity or actions to halt all dealings with them.

EXAMPLE: A potential client wants to close an open transaction quickly and offers to pay a significantly higher premium fee on the condition that your onboarding team fast-tracks the identity verification process without waiting for original documentation.

Shell Companies and Complex Corporate Structures

Obscure ownership models are a classic strategy used to mask the identity of the Ultimate Beneficial Owner (UBO), evade sanctions, and launder money. Criminals use shell companies, offshore entities, or layers of trusts across multiple countries where ownership transparency laws are weak.

The common red flags include:

- UBO cannot be identified when the company has multiple layers of ownership with no clear natural person at the top

- Nominee directors or shareholders with no apparent connection to the business

- Companies with no obvious business purpose, employees, or physical presence

- Offshore entities used in the ownership chain for UK-based assets, with no clear commercial rationale

EXAMPLE: Your business is approached by a UK limited company whose sole shareholder is an entity registered in Panama, which in turn is owned by a trust in the Cayman Islands, with no clear explanation of who actually owns or profits from the enterprise.

High-Risk Jurisdictions and International Transactions

Transactions involving countries with weak anti-money laundering controls, or high levels of corruption, or active international sanctions carry elevated risk.

The UK closely monitors international financial flows, and businesses must screen against global sanctions lists and high-risk jurisdiction indices. Thus, the Financial Action Task Force (FATF) maintains two public lists for high-risk jurisdictions:

- “High-Risk Jurisdictions Subject to a Call for Action” – the black list

- “Jurisdictions Under Increased Monitoring” – the grey list

HM Treasury translates FATF assessments into UK regulatory obligations, requiring Enhanced Due Diligence (EDD) for customers with foreign accounts in and connections to high-risk countries under Regulation 33 of the MLRs.

The red flags to watch out for include transactions or fund flows involving sanctioned countries, such as Russia, Iran, or North Korea, international wire transfers with no clear commercial purpose, especially to or from multiple countries in sequence, and the use of correspondent banks in jurisdictions with limited transparency.

EXAMPLE: A UK financial services firm receives a large transfer from a company based in a FATF grey-listed jurisdiction. The stated purpose is “consulting fees,” but no contract is presented, and the UK company has no apparent consulting activity.

Inconsistent Documentation and Source of Funds Issues

Even when documents are provided, they may not tell a consistent story. When a client’s financial profile does not align with their reported income, profession, or stated corporate net worth, it is a major compliance red flag. The same applies to falsified invoices, altered bank statements, or utility bills that look suspicious or untrustworthy.

Therefore, you should follow HMRC guidance and look out for:

- Documents that appear altered or forged

- Stated occupation or income that doesn’t match lifestyle or transaction volumes

- Source of funds that cannot be evidenced

- Third-party fund sources

EXAMPLE: A young student with no visible employment history or independent wealth attempts to purchase a commercial property worth £2 million, claiming the funds are from a vague “unspecified inheritance” but refusing to produce a certified will or probate statement.

Money Laundering Red Flags Related to Terrorist Financing Risks

There is an important distinction: money laundering focuses on hiding the origin of illicitly gained money, whereas terrorist financing is often about the destination of funds, which can come from completely legitimate sources, like salaries or even charitable donations.

Because of this, terrorist financing transaction patterns look quite different. They often involve small, unremarkable sums of money designed to fly completely under standard transaction monitoring radars.

Key money laundering risks (red flags) for terrorist financing include:

- Small, frequent transfers to individuals in conflict zones or sanctioned regions, meaning that even though amounts may be modest but the destination and frequency matter

- Transactions that appear inconsistent with any known charitable, commercial, or personal purpose

- Customers with connections to known terrorist groups and organizations. The Home Office maintains a list of such groups in the UK

- One-way payment flows with no reciprocal trade, goods, or services to justify them

- Use of cash or informal value transfer systems to avoid oversight

Under the Terrorism Act 2000 (TACT), businesses in the regulated sector have a separate obligation to report suspected terrorist financing, even if the sums involved are small.

EXAMPLE: A customer sends repeated small payments to individuals in a conflict-affected region and gives inconsistent explanations such as “family help”, “supplies”, or “business costs”. The amounts may be low, but the pattern may require escalation.

Industries Most Exposed to Money Laundering Risks in the UK

Money laundering is selective when it comes to industries it prefers to abuse. Some industries are targeted precisely because of their characteristics: high transaction volumes, cash-intensive operations, or complex ownership structures. Let’s take a closer look at the most vulnerable ones:

Financial Institutions

In the UK, banking and financial services continue to submit the overwhelming majority of suspicious activity reports in the UK, confirms NCA.

Since retail banks, electronic money institutions (EMIs), and payment service providers (PSPs) handle millions of transactions every day, they need to apply continuous automated transaction monitoring and robust Customer Due Diligence (CDD) in order to spot fast-moving illicit funds.

Overall, for financial institutions, key AML controls include:

- identity verification

- customer risk scoring

- sanctions screening

- transaction monitoring

- source of funds checks

- ongoing monitoring

Legal and Professional Services

Acting as gatekeepers of the stability of the UK’s financial system are lawyers, solicitors, accountants, tax advisors, and other professional service providers. They help clients set up companies, manage trusts, structure transactions, buy property or assets, and move money. And that makes them attractive targets for criminals seeking professional cover.

For example, only in 2023-2024, the Solicitors Regulation Authority (SRA) made 78 decisions relating to money laundering concerns and issued 44 fines totaling £556,832 for failing to act on AML red flags across three property transactions.

The most critical AML obligations for this sector include adequate CDD and source-of-funds checks before acting for clients, proper file risk assessments, and submitting SARs when criminal property is suspected.

Real Estate and High-Value Assets

The UK property market, namely high-value luxury real estate in major urban centers, is a primary target for international money laundering. Criminals use property purchases to integrate massive volumes of criminal cash transactions into the legitimate economy in a single transaction.

That’s why real estate agents, developers, and high-value dealers must enforce strict identity checks on both buyers and sellers, looking closely for hidden UBOs behind corporate purchases.

The 2025 National Risk Assessment reports that property transactions appear across money laundering typologies and offenses, including corruption, sanctions evasion, modern slavery, human trafficking, organized immigration crime, drugs, and fraud.

An example of when to enforce EDD: a buyer offers to purchase property quickly with funds from several overseas companies and refuses to clearly evidence the source of wealth.

What Businesses Should Do When They Detect Red Flags

But, identifying a red flag is only the first step. What you do next matters just as much. So, once a warning sign is flagged, your business must take structured, legally compliant actions to mitigate the risk and accurately report money laundering.

Conduct Risk Assessments and Due Diligence

When a red flag is triggered, your immediate response should be to scale up your compliance checks from standard customer due diligence to enhanced due diligence. You can do it by gathering deeper information regarding the customer’s background, verifying the exact source of wealth, and obtaining corporate proof of UBO structures.

| STEP | WHAT IT MEANS |

|---|---|

| Verify identity | Confirm the person or business is real and matches the documents provided |

| Identify beneficial owners | Understand who ultimately owns or controls the customer |

| Check source of funds | Confirm where the transaction money came from |

| Check source of wealth | Understand how the customer built their overall wealth |

| Screen for sanctions and PEPs | Identify exposure to sanctions, political influence, or higher-risk relationships |

| Record the decision | Document what was checked, what was found, and why the business proceeded or declined |

Submit Suspicious Activity Reports When Required

If your internal investigation confirms that the transaction or behavior is genuinely suspicious, you have a legal obligation under POCA to file a SAR.

In the UK, SARs must be submitted directly to the National Crime Agency (NCA) using the official online SAR Portal. If your business needs to move forward with a transaction that you suspect involves criminal property, you must submit a specific request called a Defence Against Money Laundering (DAML). You cannot proceed with the transaction until the NCA grants a clearance or the statutory moratorium period expires.

Important note: do not “tip off” the customer that a SAR has been filed or that they are under investigation, because doing so is a criminal offense under POCA.

Unlike some jurisdictions, the UK has no general minimum exemption for SARs – the threshold for reporting is suspicion itself, not a transaction’s size. However, a threshold amount applies in specific account-operating contexts, currently £3,000 following an increase in July 2025.

Maintain Ongoing Monitoring Processes

AML compliance is a continuous process, because customer risk changes over time.

A client who looked safe two years ago could suddenly develop a high-risk profile today. For example, a customer who was low risk at onboarding may become higher risk if they start trading internationally, change beneficial ownership, receive unusual payments, or begin using new products.

Therefore, you should maintain an active, continuous monitoring process that periodically reviews transaction behaviors against a customer’s known risk profile, updating documentation whenever significant changes occur.

Effective ongoing monitoring includes:

- Regular review of customer risk ratings, especially when circumstances change

- Transaction monitoring against expected behavior – flagging deviations from baseline patterns

- Screening against sanctions lists, Politically Exposed Persons (PEP) and adverse media databases at regular intervals and whenever those lists are updated

- Periodic re-verification of customer identity and source of funds for higher-risk relationships

How Automation Helps Detect Money Laundering Red Flags

Here is how a manual AML compliance nightmare looks like: checking every single UK company filing, tracking changing global sanctions lists, and calculating complex transaction patterns across thousands of accounts – all by hand.

Not to mention that manual AML checks can leave your business highly vulnerable to human error and backlogged compliance pipelines.

The answer to all this trouble is AML automation!

Modern AML technology can monitor transactions 24/7, screen customers against global sanctions, adverse media and PEP databases in seconds, generate risk scores dynamically, and flag anomalies that a human reviewer might miss across thousands of data points.

Automation does not replace human judgment. Instead, it makes judgment easier by giving compliance teams clearer alerts, better context, and fewer blind spots. Also, for regulated businesses dealing with significant customer volumes, automation is simply a necessity.

Here’s how manual and automated approaches compare across key compliance tasks:

| Detection method | Manual verification processes | Automated compliance solutions |

|---|---|---|

| Processing speed | Slow – requires manual documentation reviews and individual lookups. | Instant – runs real-time database checks and automated identity parsing. |

| Human error risk | High – compliance teams can easily overlook complex corporate layers or typos. | Minimal – rule-based workflows process every single data point identically. |

| Sanctions & PEP screening | Periodic or ad-hoc checks – leaves gaps between regular scheduled reviews. | Continuous – provides live, automated alerts whenever global lists update. |

| Audit trail tracking | Scattered – relies on manually filed spreadsheets, emails, and local drives. | Centralized – stores comprehensive, time-stamped digital logs for regulators. |

| Scalability | Expensive – requires hiring more staff to handle growing transaction volumes. | High – handles spikes in volume effortlessly without expanding headcount. |

For example, a solution like Ondato can help businesses combine identity verification, business verification, risk scoring, screening, and monitoring into one workflow, making it easier to detect red flags early without slowing down legitimate customers.

Our comprehensive automated compliance suite is designed to take the complexity out of UK AML requirements. By integrating real-time IDV checks, KYC/KYB screening, continuous PEP, adverse media, and sanctions monitoring directly into your existing business systems, we help you detect money laundering red flags instantly.

Contact our compliance experts today to see how our automated solution can optimize your risk management strategy.

FAQ