The Role of KYC Law in Law Firm Compliance

The legal industry is no exception to the global push for stricter Anti-Money Laundering (AML) and counter-terrorist financing rules. Law firms are increasingly required to adopt Know Your Customer (KYC) procedures to verify client identities, assess risk, and monitor ongoing relationships. While the exact obligations differ by jurisdiction, they all share the same principle: a risk-based compliance approach designed to prevent financial crime and protect the integrity of the legal profession.

Legal AML Requirements for Law Firms

The main reason law firms need to implement KYC is simple: they, like every other business that deals with the transferring of money, must adhere to Anti-Money Laundering (AML) regulations.

In the US

Law firms that engage in financial transactions, such as handling client funds or setting up corporate entities, fall under the Bank Secrecy Act (BSA) and related AML obligations. Although the proposed Enablers Act (drafted after the Pandora Papers scandal) did not pass, it highlighted lawmakers’ intent to bring stricter AML/KYC oversight to law firms. Many states already impose requirements that align with global standards, and further reforms remain likely.

In England

Under the Money Laundering Regulations 2017, law firms must conduct KYC checks on all clients and maintain updated records through ongoing monitoring. Oversight is provided by the Solicitors Regulation Authority (SRA), which has the power to fine firms, revoke licenses, and issue public disciplinary actions against non-compliant practices.

In New Zealand

Law firms are subject to the Anti-Money Laundering and Countering Financing of Terrorism Act (AML/CFT Act). Any practice acting as a formation agent for companies or managing client funds must perform full AML procedures, including KYC identity verification and beneficial ownership checks.

In the EU

The EU’s AML Directives (from the 4th to the current 6th AMLD) require law firms to apply KYC when handling high-risk transactions, setting up trusts or companies, or managing client money. These directives establish a harmonized framework across member states, ensuring that law firms across Europe share the same baseline of AML/KYC compliance obligations.

Does Your Law Firm Need KYC?

The short answer: yes. Whether legally mandated or strongly advised, KYC is essential for law firms. It allows them to comply with global standards, manage risk effectively, and build stronger customer relationships. In practice, KYC is part of a broader framework that includes customer due diligence (CDD), enhanced due diligence (EDD) for higher-risk clients, and ongoing monitoring of customer risk profiles. Together, these measures protect law firms from exposure to financial crime and ensure they operate with confidence.

Avoiding Fines

Failure to comply with KYC and AML regulations can result in severe penalties. For example, in 2022 a UK law firm was fined £20,000 for non-compliance, and in 2023 alone, 49 firms in the legal sector faced similar sanctions. Just as the Financial Industry Regulatory Authority (FINRA) enforces strict rules in the financial sector, regulators overseeing the legal profession are increasingly imposing fines and disciplinary action. For law firms, compliance is not optional — it’s a safeguard against financial disruption and reputational loss.

Risk Assessment

Conducting thorough customer due diligence allows law firms to identify and assess customer risk profiles before entering into an engagement. This includes verifying client identities under a Customer Identification Program (CIP), screening for sanctions, politically exposed persons (PEPs), and reviewing reputational risk through adverse media checks. For higher-risk clients or complex structures, firms must apply enhanced due diligence to gain a full understanding of ownership, funding sources, and potential exposure to financial crime. Ondato’s solution simplifies this process, helping firms make informed decisions with confidence.

Financial Crime Prevention

Money laundering and terrorism financing are persistent global threats — and law firms can be misused as intermediaries without strong safeguards. Implementing robust KYC procedures ensures that suspicious transactions are detected early, minimizing exposure to illegal activity. By combining ongoing monitoring with risk-based controls, law firms can protect their financial stability, reduce the chance of regulatory breaches, and demonstrate commitment to preventing crime.

Reputation Credibility

Law firms are trusted advisors, and their reputation depends on safeguarding both compliance and client data. By implementing reliable KYC processes, firms reinforce trust in customer relationships while assuring regulators and clients alike that they are serious about preventing financial crime. A firm known for strong compliance practices is better positioned to attract clients, retain business, and avoid the reputational damage that comes with being associated with money laundering or terrorism financing.

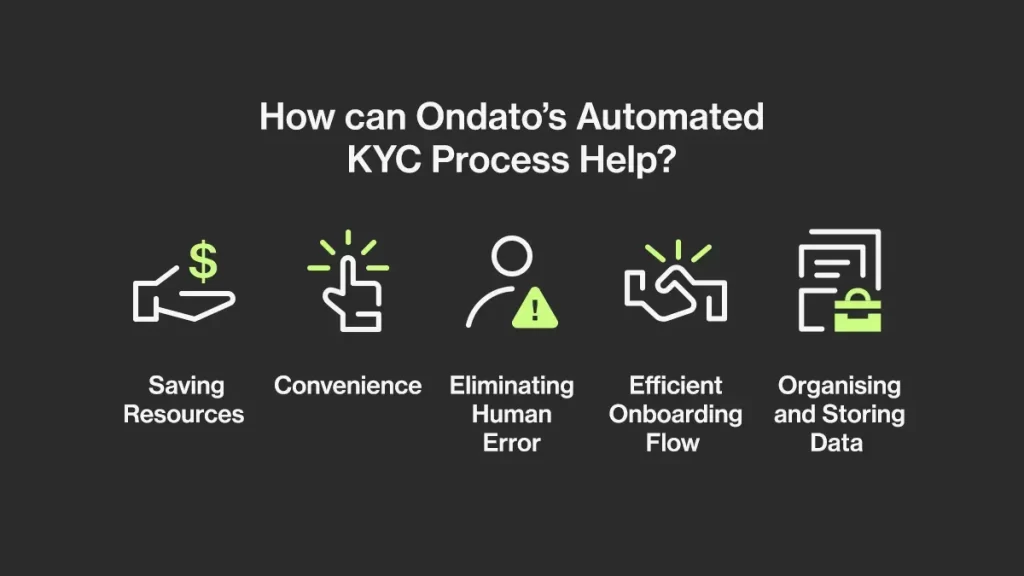

Benefits of Ondato’s Automated KYC for Law Firms

For law firms, efficiency is just as critical as regulatory compliance. Time-consuming manual checks can slow down client onboarding, drain resources, and create unnecessary risk. Ondato’s automated KYC for legal entities and individuals is designed to streamline verification, giving law firms the tools to stay compliant while focusing on their core services. By combining AI-driven technology with a risk-based compliance framework, Ondato helps firms reduce operational strain, cut costs, and deliver a seamless experience to clients.

Saving Resources

Manual KYC checks often require large compliance teams dedicated to verifying identities, reviewing documents, and storing records. These tasks consume significant time and budget, especially for firms handling high volumes of clients. Ondato automates identity verification and monitoring, freeing up valuable staff hours and reducing overhead. Instead of scaling costs with headcount, law firms can scale compliance with technology — keeping budgets predictable while improving accuracy.

Convenience

Ondato’s solution is designed to be simple and adaptable. Law firms can implement it with minimal integration requirements, avoiding lengthy IT projects and ensuring a fast setup. The system is flexible enough to support both boutique firms with modest client volumes and global practices managing thousands of cases. This convenience extends to clients as well: onboarding is smoother, faster, and requires fewer manual steps, making the process less intimidating and more user-friendly.

Eliminating Human Error

Even the most skilled compliance teams are not immune to mistakes, particularly under pressure from long hours and heavy caseloads. Errors in KYC can lead to missed red flags or regulatory breaches. Ondato’s AI-driven checks work with consistent accuracy, reducing the likelihood of oversight caused by fatigue, stress, or manual missteps. By automating repetitive verification tasks, law firms can trust that every client is screened with the same high level of scrutiny.

Efficient Onboarding Flow

Traditional onboarding in the legal sector is often drawn out, involving multiple back-and-forth exchanges, document requests, and in-person verification. Processing a single corporate client manually can take weeks or even months. With Ondato’s automated workflows, this process is condensed into just a few steps, often completed within days. The result is a smoother client journey, faster revenue recognition for the firm, and reduced frustration on both sides.

Organising and Storing Data

Paper-based or fragmented digital recordkeeping poses significant risks: documents can be misplaced, destroyed, or difficult to retrieve when needed for audits or investigations. Ondato centralises all KYC data in a secure, digital environment that is compliant with data protection standards. Law firms can instantly access client records, generate reports, and demonstrate compliance to regulators without the hassle of manual searches. This not only increases efficiency but also strengthens resilience against data loss and reputational risk.

FAQ